Strategizing from 7 cities across the globe

Reverse Solow: The Long Run Curse of Lebanese Investment

While Israel has been facing considerable losses, those are not comparable to Lebanon’s casualties. A state that was just reconstructing from a devastating financial crisis found its Solow process being reversed backward. Using an economic perspective, we can witness the overall fall of the Lebanese Solow Model, reflecting the meaning of war on an investment basis, and the curse carried upon the workforce.

MIDDLE EASTECONOMICSTRADEINVESTMENTWAR

Elie Joe Akiki, Ali Dagher

10/22/20246 min read

They say that by the end of a war, no winners can be identified, but only losses due to the fall of diplomacy and the rule of law. As the war on Lebanon started a month ago, the consequences exacerbated progressively, with the displacement of over 1.3 million people and the breakdown of Lebanese infrastructure. While Israel has also been facing considerable losses, those are not comparable to Lebanon’s casualties. A state that was just reconstructing from a devastating financial crisis found its Solow process being reversed backward. Using an economic perspective, we can witness the overall fall of the Lebanese Solow Model, reflecting the meaning of war on an investment basis, and the curse carried upon the workforce. This piece endeavors to reflect the detriments of the war upon the Lebanese investment equilibrium, portraying its influence on the integral population despite affecting some more than others.

The Solow model is an economic analysis that tackles the stable level of capital for a certain country. It merges the overall demand for investment – or in other words, the willingness to pay for extra capital of a country – and depreciation – the amount of infrastructure that gets malfunctioned due to time or certain events.

Let us take a look at the Lebanese Solow Model to be able to assess the current capital and what would happen within the war.

The Investment equation is written as follows assuming a Cobb-Douglass equation:

so investment per capita is

Where r is the real interest rate, L the labor force, K the current capital, the share of capital within the production, A is a certain technology index, and finally δ the depreciation rate of capital. Knowing most of the variables we will have the following equation:

According to the Solow model, the economy would be equal to the total deprecation. As it explains, investment is increasing at a decreasing rate, while the overall depreciation increases with capital at a steady state. This means that up to a point, the investment and depreciation would cancel out each other over and over, leading to what we call the “Long Run Steady State” of capital.

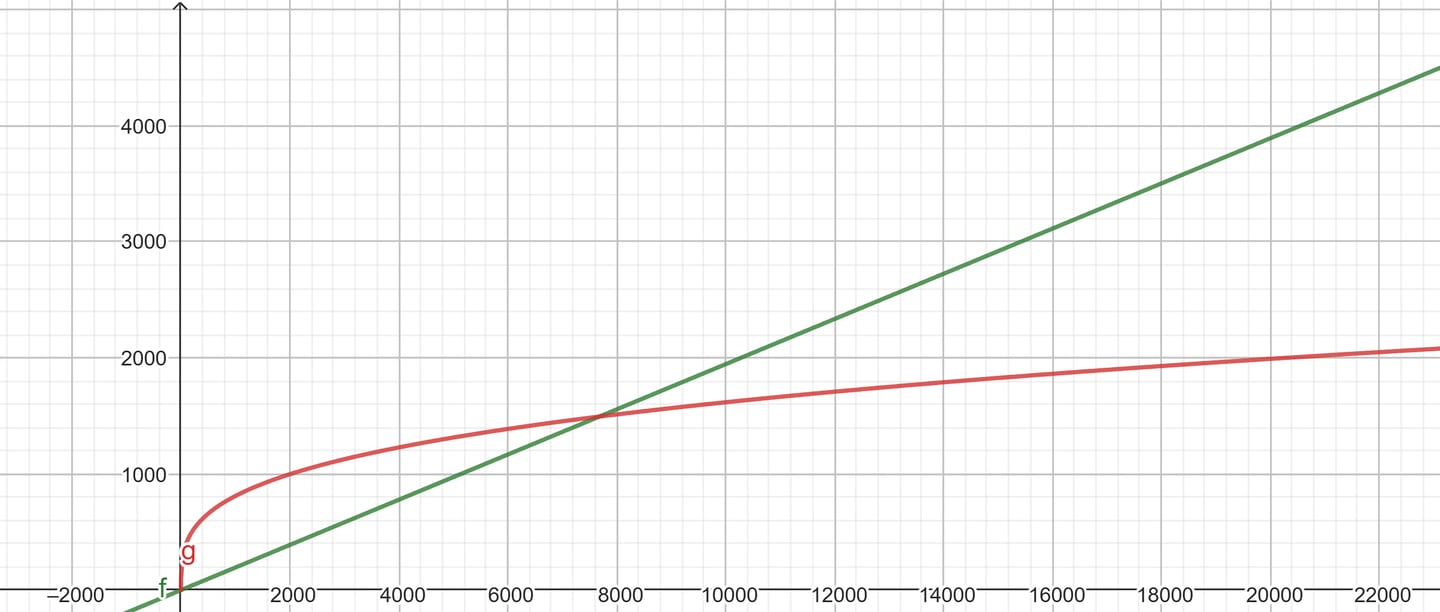

This being mentioned, we can get the depreciation rate by i= δ*k which would give us a total depreciation rate of 19.46% before the start of the war and an investment per capita of $1494 without considering the foreign direct investment.

The equilibrium for investment and the depreciation equation would give us the following graph

The intersection here gives us a steady rate, and while the destruction of capital would lead to extra investment, we are still extremely far away from getting back to our new state.

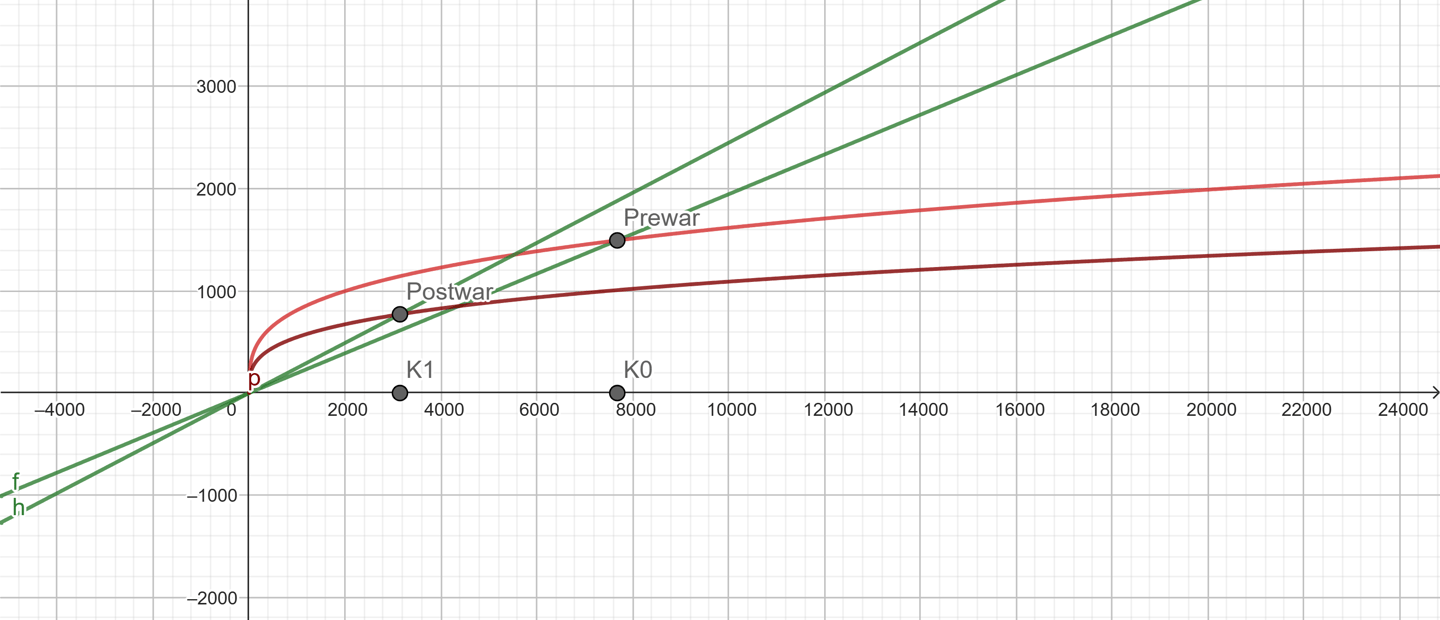

So what happened with the war? The core idea is that the extreme bombings did not only cripple the infrastructure of the country, but they also created a war risk probability, which would be accounted for in depreciation as well. The new capital would be an expectation E[K]= (1-P)K +P*r*K where P is the probability of getting bombed, currently increasing due to the tensions, and r is the rate of destruction. Hence, (1-P)K is the expectation in case of no bombing and P*r*K is the expectation in the case of bombings taking place.

This being said, the depreciation rate increased due to the massive risk of annihilation, causing a shift within its slope. The destruction of the infrastructure would not be easy to rebuild. Thus, the steady state is already at a lower level.

Now, if we consider what happens to investment demand, the war risk premium would result in a drawback in the willingness to invest in the country. Not to be outdone, the current wave of brain drain would obviously lead to a technological regression. As the specialized labor capable of working abroad is leaving the country whenever opportunity prevails, the overall knowledge of production in the country decreases, and therefore lowers the willingness to invest.

On top of that, the discouraged labor effect is happening on a psychological level, where the managerial strategies are not as reliable anymore. The discouraged labor would not be able to think as rationally as before considering the constant distraction and priorities of concern taking over the benefit of producing, triggering another technological downfall within the nation. The consequences of the war would decrease the marginal product of Labor, not only on a technology level but also on a capital level.

All in all, we can witness an aggregate decline, which can also be due to a possible increase in military spending, being a core drawback to economic growth in terms of Middle Eastern countries. A certain increase in military spending would cause a “Crowding Out Effect” on the country. As the increase in spending cannot be achieved without a certain increase in revenues – which is most probably coming from taxation – this would cause a lesser marginal benefit on capital, leading to another regression of the investment curve.

Here is a module that would show a change of these variables. While it is hard to estimate the change in depreciation and investment demand, we can rest assured that our capital level in the steady state is going to decrease.

However, we anticipate that some countries, particularly neighboring Arab nations that remained silent during the war in Lebanon, will step in to contribute to the country’s reconstruction. Unfortunately, rather than acting out of genuine goodwill, these countries (especially Qatar, the UAE and Saudi Arabia) are likely to offer aid in exchange for access to Lebanon’s untapped oil reserves.

These nations are well aware that Lebanon lacks the financial resources and infrastructure to extract its own oil, and they see the country’s vulnerable position as an opportunity to bolster their own oil reserves and obtain a good status in the eyes of the United Nations and the rest of the world. It is also worth mentioning the leverage that they will possess by hiring Lebanese labor, which is rather well trained, thus creating a boom for their economy. As the economic competition between the UAE and Saudi Arabia is getting more and more tense, the Lebanese labor may adjuvate one of these two to become the hub of Economic growth for the Arab world.

In conclusion, it was no secret that the investment in the country after the war would decrease, and the economic consequences are severe. The Solow model reflects a long run curse in Lebanese investment, which would affect the integral population regardless of its division. In the end, the Solow model reflects the poorer standard of living that Lebanon must face after a ceasefire, where hard work and a long time to go are required in order to get back to our original point. Despite having certain populations more affected than the others, the war will financially impact us all. Although we acknowledge how this situation affects our capital rate, we must also realize that wages and labor are not immune to war either.

References

Collier, P. (1999). On the Economic Consequences of Civil War. Oxford Economic Papers, 51(1), 168–183. http://www.jstor.org/stable/3488597

Knight, M., Loayza, N., & Villanueva, D. (1996). The Peace Dividend: Military Spending Cuts and Economic Growth. Staff Papers (International Monetary Fund), 43(1), 1–37. https://doi.org/10.2307/3867351

World Bank. (n.d.). Real interest rate (%) [Data set]. World Bank Group. Retrieved October 16, 2024, from https://data.worldbank.org/indicator/FR.INR.RINR?locations=LB4o